Addressing supply-chain emissions enables many customer-facing companies to impact a volume of emissions several times higher than they could if they were to focus on decarbonizing their own direct operations and power consumption alone. By implementing a net-zero supply chain, companies enable emission reductions in hard-to-abate sectors, and accelerate climate action in countries where it would otherwise not be high on the agenda. A net-zero supply chain is also possible with very limited additional costs, a new report of World Economic Forum and BCG shows.

The Big Eight: eight supply chains account for more than 50% of global emissions.

Food, construction, fashion, fast-moving consumer goods, electronics, automotive, professional services and freight account for more than half of all global greenhouse gas emissions. A significant share is indirectly controlled by only a few companies. Only a small proportion of these emissions are produced during final manufacturing. Most are embedded in the supply chain—in base materials, agriculture, and the freight transport needed to move goods around the world.

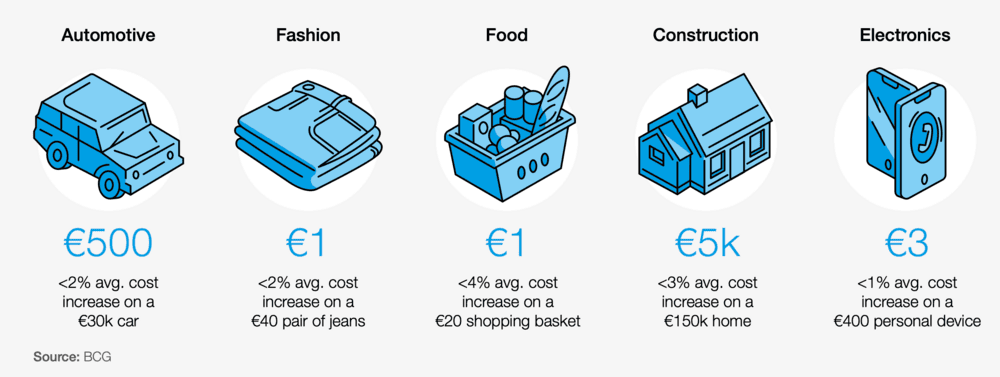

Net-zero supply chains would hardly increase end-consumer costs.

For producers of many of these materials, as well as for freight transport players, ambitious decarbonization is extremely challenging. Many emission reduction measures are comparatively expensive. Supply chain partners often operate in markets that are commoditized, with slim margins and limited opportunities for differentiation. Across a whole value chain, however, emissions may be addressed more affordably. In most supply chains, there is the potential for substantially more efficiency and for much greater reuse of materials. In addition, a large share of emissions comes from traditional power, which can be replaced relatively cheaply with renewables.

Around 40% of all emissions in these supply chains could be abated with readily available and affordable levers (<€10 per tonne of CO2 equivalent), such as circularity, efficiency and renewable power – with only marginal impact on product costs. As a result of this—and the fact that emission-intensive base materials account for only a small share of end consumer prices—decarbonization is much less expensive for companies at the end of any given value chain. Even with zero supply-chain emissions, end-consumer costs would go up by 1–4% at the most in the medium term.

How can this be? As an example, consider the steel that goes into a midsize family car with a $35,000 sticker price. Producing steel is one of the most emissions-intensive activities in the supply chain. Producing zero-carbon steel can increase the steel makers’ costs significantly—by as much as 50% in some cases. But since steel accounts for only roughly $1,000 of total car costs, the markup on this final product will be much, much lower. In fact, the same car made with exclusively zero-carbon materials would cost only about $600 more—or roughly a difference of 2%. Considering that getting there will take even the most ambitious companies many years, the immediate economics look much less scary.

But decarbonizing supply chains is hard

Even leading companies struggle to get the data they need and to set clear targets and standards to which their suppliers must adhere. Engaging an often-fragmented supplier landscape is challenging – especially when emissions are “buried” deep in the supply chain, or when addressing them might require collective action at the industry level.

While a manufacturer can calculate the greenhouse gas emissions from its own operations with a relatively high degree of confidence, getting a view on scope 3 emissions is complex. The challenges are especially daunting for companies with tens of thousands of individual products and significant turnover in the supplier base. Some even struggle to understand who their suppliers are in the first place. It does not help that data-sharing on product emission footprints is still in its infancy.

Even when companies have a decent amount of transparency, addressing emissions is far from trivial. Supply chain emissions can be distributed across hundreds of individual tier n suppliers (including suppliers and suppliers of suppliers) in many countries around the globe. They are not static. And prompting action can be challenging. It requires a deeper understanding of abatement economics in upstream sectors, more intensive engagement with suppliers, greater education, joint projects, and, in some cases, the willingness to commit to long-term partnerships. Not many procurement organizations are set up to do these things.

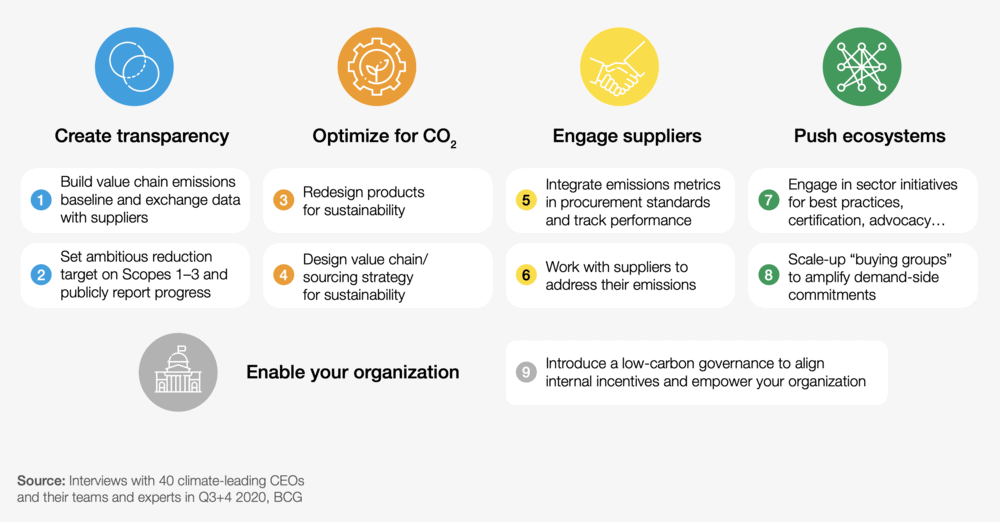

Nine major initiatives every CEO should push for to reach Net-Zero

Through interviews with several dozen global companies that lead the way in reducing supply-chain emissions, nine key actions were identified to overcome barriers:

- Build a value chain emissions baseline and exchange data with suppliers. Establishing a comprehensive emissions baseline is a crucial first step. Starting with tier 1 suppliers and the products, components, and commodities that account for the most CO2 emissions, companies should define a baseline using emissions factor databases, paired with direct supplier data where available.

- Set ambitious reduction targets on scopes 1 to 3 and publicly report progress. Once they have transparency on their supply chain emissions, companies should set a public target of 1.5°C, a net-zero target, or both, across all emissions scopes and understand what this means for their businesses. In most cases, targets are achievable at limited cost. Companies should also actively cascade targets through their supply chains.

- Redesign products for sustainability. Companies should make sustainability part of design decisions, for example by increasing recyclability and using greener materials. Even existing products can be redesigned to reduce supply chain emissions.

- Design the value chain and sourcing strategy for sustainability. Companies should also consider emissions in their value chain design choices, for example by rethinking their make-or-buy decisions and by limiting the need for long-range logistics. Nearshoring can reduce transport emissions and has the secondary benefit of making supply chains more resilient to shocks—increasingly important in a postpandemic world.

- Integrate emissions metrics in procurement standards and track performance. Setting procurement standards for suppliers is one of the most powerful direct ways to address upstream emissions. Strong standards link practices to procurement decisions, such as mandating a specific share and quality of renewable power, required levels of process efficiency, or a required share of recycled materials. In some cases, this may require more intensive engagement—for example to educate, provide technical advice, enable longer-term asset upgrades, or encourage a commitment to continuous improvement.

- Work with suppliers to address their emissions. Some upstream suppliers may lack the knowledge to reduce emissions. Providing education and technical support can be transformative. Where tier n suppliers struggle with the economics of longer-term asset upgrades, companies can help by co-investing or committing to longer-term offtakes.

- Engage in sector initiatives for best-practice sharing, certification, traceability, and policy advocacy. Pushing for sector initiatives through industry bodies is another way to increase impact. Ambitious companies should put pressure on industry bodies and other organizations to establish sector-level targets for climate action. Companies can also join forces in cross-sector policy groups to change the wider policy context for decarbonization.

- Scale up buying groups to amplify demand-side commitments. Joint commitments on green materials can be a powerful tool to encourage upstream investments into otherwise subscale decarbonization technologies and make green solutions more economic over time.

- Introduce a low-carbon governance to align internal incentives and empower your organization. Finally, companies looking to decarbonize their supply chains need to change the way they operate internally. Procurement functions will have to adjust, as will product development, finance, strategy, and sustainability. Supply chain changes will be successful only to the extent that they are supported by clear targets, dedicated funding, and management incentives. At the same time, the number of interfaces between functions involved in climate-related topics needs to be reduced. All of this requires better governance.

It is time to move!